The UK energy industry has made impressive progress on clean energy. Renewable generation is up, carbon emissions are falling, and the political commitment to a clean power system by 2030 is clear. The retail market that will deliver change in customers’ homes and businesses was designed for a different time and is no longer fit for purpose.

We recently worked with Energy UK on a report, Demand Better, exploring whether the retail market was ready to deliver government policy ambitions such as Clean Power. We asked energy suppliers, flexibility service providers, technology companies, former regulators and consumer representatives what they thought of the progress, pitfalls and potential solutions.

The response was overwhelming; the retail market is broken. It was built for a world of commodity supply where affordability and competition were the primary goals - not one prioritising flexibility, innovation and consumer engagement in the energy transition. Worse still, current structures are actively preventing the changes needed to meet our energy policy ambitions.

Our conversations highlighted widespread agreement on the challenges facing the sector as well as some healthy disagreement on the solutions needed – though with some recurring ideas. Our report presents clear recommendations where the evidence supports a definitive and positive solution.

Why it’s important to raise this now

Government energy policy ambitions require widespread consumer adoption of low carbon technology as well as changes in the way customers use energy and engage with the wider market. Without a functioning retail market capable of innovation, earning consumer trust and attracting long-term investment, these ambitions the transition will fail, regardless of how much progress we make elsewhere. We’ve developed this report to stimulate discussion and influence decision-makers at the highest level to act before it’s too late.

Delivering the clean energy transition requires immediate retail market reform.

Retail market reform is not a secondary consideration for the clean energy transition but a critical enabler.

The potential savings if we get this reform right are significant. Achieving clean energy targets through retail market innovation could deliver between £30bn and £70bn in consumer savings by 20501. But realising those savings requires suppliers to invest in flexibility platforms, dynamic tariffs and bundled propositions. Current market structures prevent that investment.

Four barriers blocking progress

From the extensive industry engagement, we identified four interconnected barriers holding the market back.

1. Regulatory burden and complexity

We’ve reached unsustainable levels of regulation. Supply licence conditions and industry codes total nearly 10,000 pages. Ofgem’s preference for input-based regulation mandates specific systems and processes rather than the outcomes they’re supposed to deliver. This deters investment, adds cost (serving a UK customer costs more than double the equivalent in France) and makes it difficult for new business models to operate.

Ofgem will say ‘we won’t give you guidance’ but are then quick to enforce when you get it wrong.

Head of External Affairs

Outcomes-based regulation, the approach the FCA has successfully moved toward, offers a better path; defining what consumers should receive and then letting providers compete over how best to deliver it.

The prices of becoming a licenced supplier (in regulatory burden and reputational risk) means investors have stayed away when they might have been quite helpful disruptors.

Former Director of a new entrant

2. Short-term firefighting

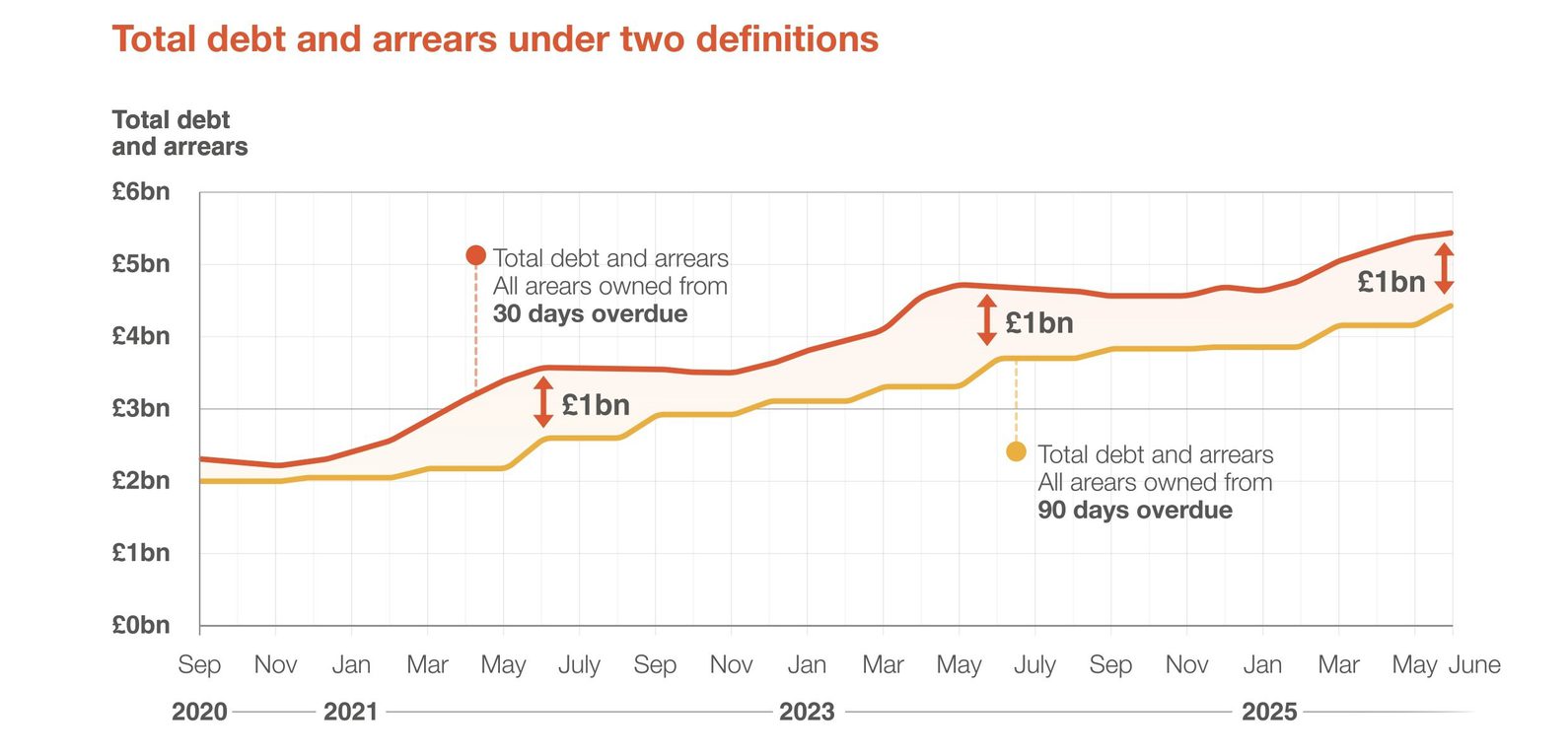

Consumers owe energy suppliers approximately £4.5bn today – and rising. Managing that debt consumes substantial supplier resource which is shifting focus away from innovation and progress.

A typical household is now paying around £70 a year to cover debt-related costs across the industry. And price cap mechanics absorb management time further on hedging, forecasting and regulatory compliance.

The pressure is always on addressing some operational issue like the level of customer debt. It’s difficult to get people to look beyond short-term issues.

Director of Strategy

It’s entirely rational for organisations to manage immediate risks so this isn’t a failure of individual companies. But what’s rational at organisational levels creates risks at the national policy level. In particular, we lose management time and capital which would be better used developing long-term capabilities.

3. Distributional inequalities

Millions of households across the country face barriers to the low-carbon and cost-saving benefits that the energy transition could deliver. There are too many barriers for consumers which pricing propositions can’t address.

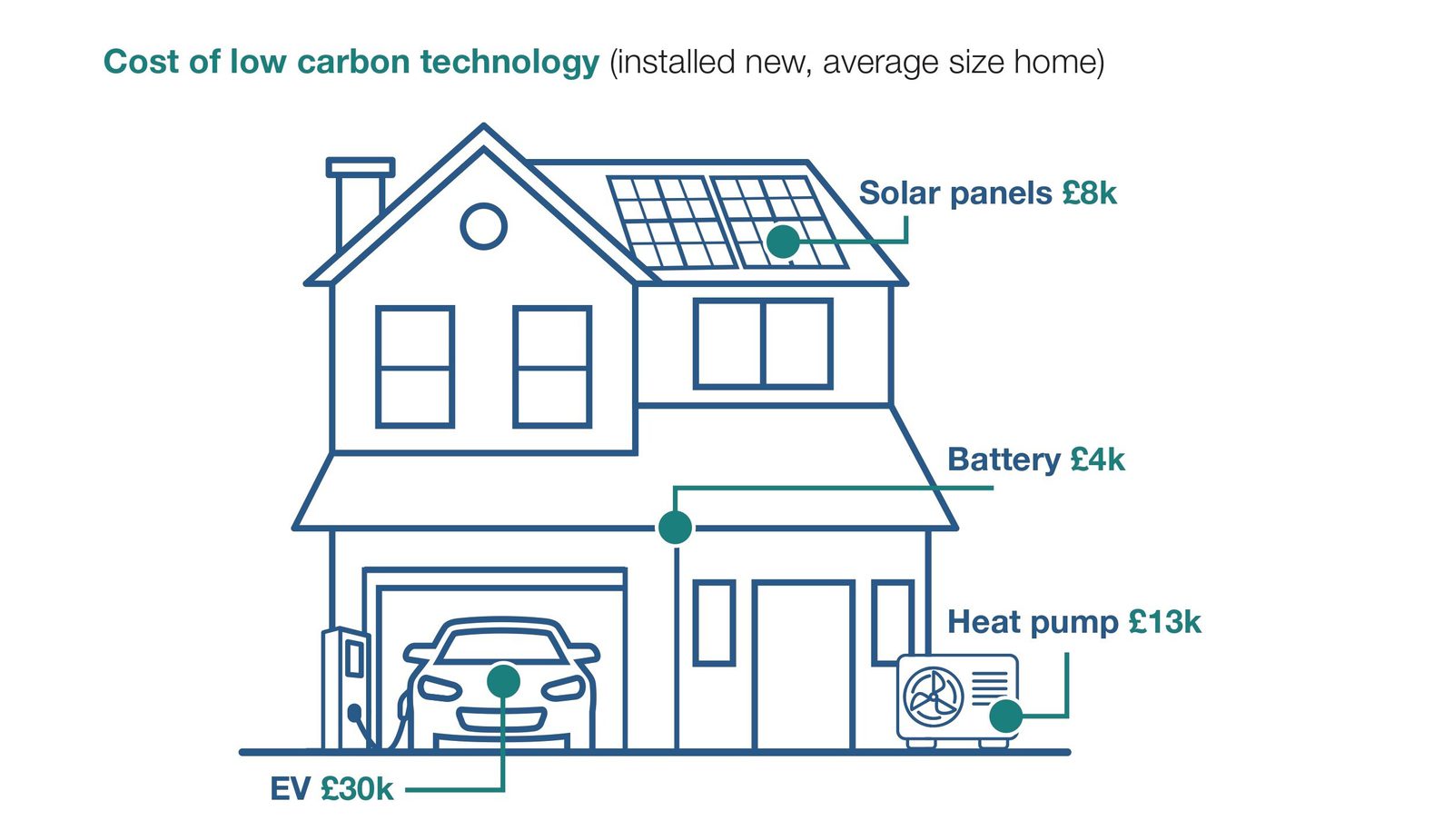

We estimate 5.4m private rental households couldn’t install heat pumps or EV chargers regardless of how attractive retail offers become. Landlords investing in low-carbon technology reap little rewards as the savings are typically for the bill-paying tenants. This incentive gap between capital investment and operational savings creates a structural barrier for all low-carbon options.

On top of this, an extra 1.5m households lack internet access, with a further 2m or more with inadequate devices, unaffordable data or poor digital skills, which flexible tariffs rely on.

The result of these various barriers is the systematic exclusion of ~20% of all households from flexibility markets.

Flexibility targets also assume millions of customers will adopt smart tariffs and automated services, but awareness remains low. Fewer than 30% of existing EV owners understand the potential savings from smart charging. Creating consumer pull through awareness and trust-building is as essential as creating supply-side capability.

This is compounded by the up-front of key low carbon technologies. Even with government subsidies low-carbon technologies such as, solar panels, batteries, EV and heat pumps, remain too expensive for most households.

If the market continues with the current structure, the energy transition risks creating a two-tier system. Affluent early adopters who are willing and able to invest will benefit from low-carbon technology and flexible products, while those who aren’t bear the burden of the distributed costs.

Innovation is effectively limited to the engaged

Chief Commercial Officer

4. Pricing constraints

Current pricing structures limit innovation and investment opportunities. Consumers need markets that enable flexibility services, technology adoption and dynamic pricing, which isn’t available today.

The commodity-focused price cap restricts demand for, and therefore the development of, the dynamic tariffs, time-of-use pricing and bundled services essential for flexibility. Plus, it doesn’t go far enough to ease the burden on the most vulnerable, while restricting what suppliers can develop or offer.

The price cap is hugely complex and very restrictive. The allowed margin is very low and if customers don’t pay, you’re losing money. This isn’t investible.

Director of Strategy

By limiting the potential profits and capital for long-term investment, the industry remains focused on tackling short-term problems. Combined with the ongoing management challenges of rising debt levels, suppliers and consumers are stuck where they are.

Finally, more than 50% of an average household bill is made up of pass-through charges that suppliers cannot influence. When suppliers lack pricing power over most of the bill, their ability to design attractive propositions is severely limited. All of this means there’s a disconnect between what the industry needs to develop, what consumers want and what suppliers can deliver. The future pricing system must work with propositions that optimise consumption and reduce consumer or supply friction.

There’s a lack of competitive headroom in the price cap, meaning suppliers just aren’t incentivised to deliver the propositions that we need to see.

Head of Regulation

Recommendations for improvements

During our conversations compiling the report, we had plenty of discussion about the problems, but more importantly, enthusiastic ideas for potential solutions.

We distilled the ideas down to 23 evidence-backed recommendations in the report – each with clear benefits. Whilst we encourage you to read the full report we have listed several of the key proposals below.

The most pressing suggestions highlighted the need for regulation to shift toward outcomes rather than inputs, a structural solution to debt (not a one-off scheme), addressing the consumer barriers to participation and restoring the pricing power suppliers need to innovate.

Tackling regulatory burden and complexity

We’ve compiled nine recommendations for regulatory change, as this is the biggest hurdle to the energy future we need. Three examples include:

- A comprehensive supply licence review, with a binding commitment to reduce regulatory burden and refocus on consumers, investment and Clean Power.

- Standards should be measurable, achievable and genuinely linked to consumer benefits.

- Regulation should apply to services, not business types, with fair competition across all market participants offering each service.

The net effect of the changes we recommend would be to enable suppliers and retailers to focus resources on actually building future capabilities rather than demonstrating compliance. It would help new entrants compete based on service quality and efficiency, with better customer outcomes along the way. And it would encourage the investment decisions we need to see if we’re to deliver on our ambitions for energy policy.

Avoiding short-term firefighting

Our report contained recommendations that included:

- Address both existing debt burdens and prevent future accumulation.

- Enable planning for consumer propositions.

- Free up (retailer/supplier) resources for customer-facing innovation.

- Deliver potential bill savings and better investment in the platforms required to deliver those savings.

Together, we argue enacting these changes would help suppliers focus more attention on building the innovative products, propositions and partnership necessary to break down the barriers to low carbon technology adoption and engage customers on making the positive changes we need to see.

Addressing distributional inequalities

Our report set out five recommendations that address this, including a higher minimum energy performance standard for rental properties, on-bill financing schemes for low-carbon adoption and improving digital access and skills.

Adopting these changes would have significant benefits, within and beyond the energy sector. These would include a fairer distribution of the costs and benefits from delivering the energy transition as well as breaking down the structural barriers to engagement that exist today.

Relaxing pricing constraints

We made six recommendations here including the removal or evolution of the price cap to a more targeted scheme designed to protect those consumers who are genuinely unable to pay, meaningfully different peak and off-peak rates to incentivise demand shift and recovery of energy policy costs through taxation instead of on-bill funding.

Adopting these recommendations would have material benefit. Together, they would help create an opportunity for greater support for vulnerable consumers whilst simultaneously developing space for innovation across the market. They would restore pricing power, essential for flexible market innovation, whilst also reducing system costs and consumer bills.

A concerted effort

The retail energy market has served us well but is ill-suited to the job now at hand. Delivering our energy policy ambitions will require us to rethink our approach to retail market regulation, and that will need concerted action from government, Ofgem and industry. We can’t address any of these barriers in isolation. Adapting now will reduce costs, enable innovation and deliver a fairer transition for everyone. Delaying will make everything harder and more expensive.

At BFY Group, we work with organisations across the energy retail market every day. Our clients are wrestling with the challenges described in this report. The £4.5bn debt burden, the compliance overhead, the difficulty of making new propositions stack up financially under current structures.

The recommendations in Demand Better reflect a genuine consensus across the sector. We’re proud to have contributed to this report alongside Energy UK, and we’d encourage anyone with a stake in the sector’s future to read it in full, engage with the debate and champion urgent change.

Read the full Demand Better report.

Get in touch to discuss any of the barriers or what these recommendations mean for your organisation.