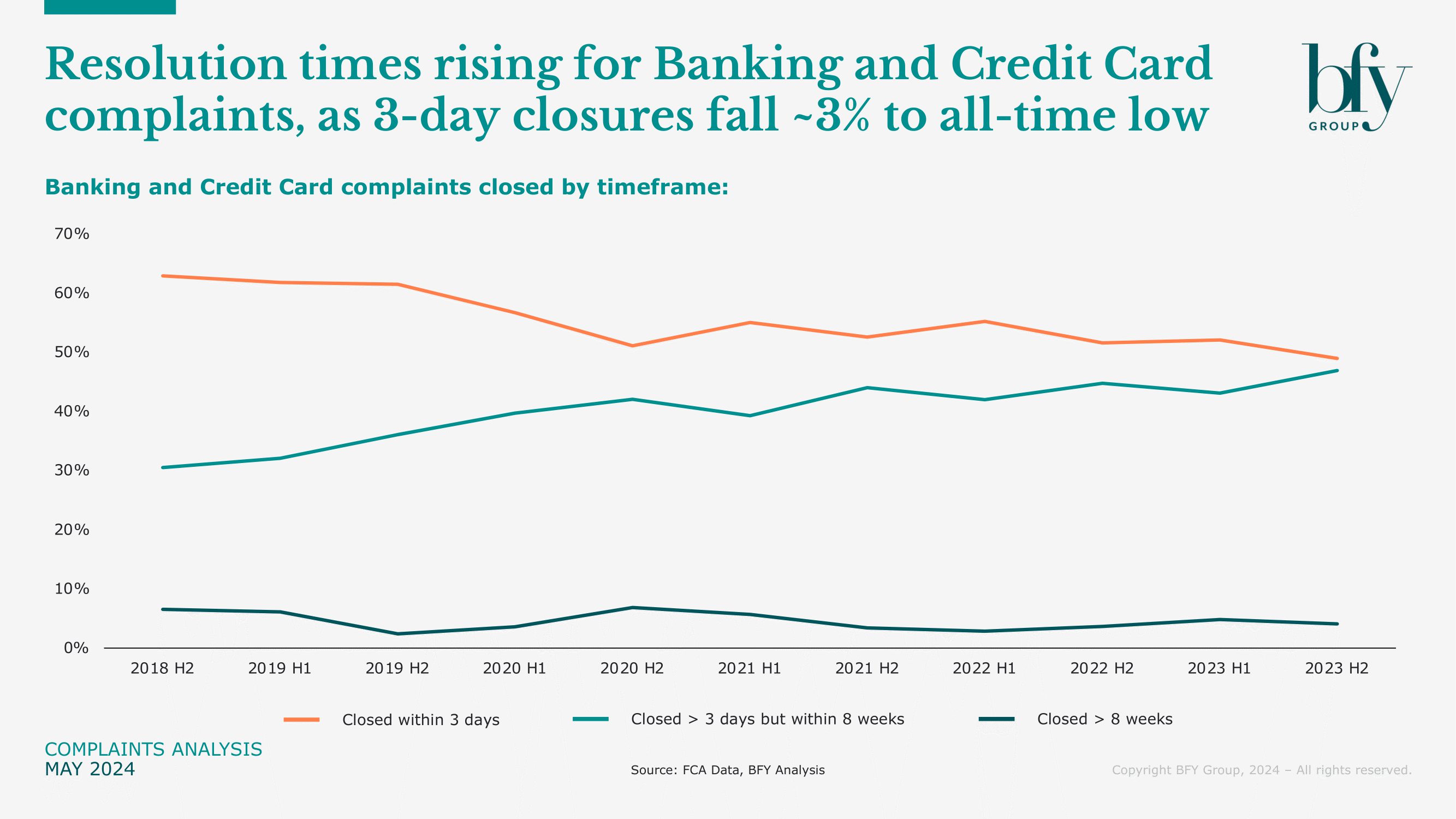

FCA’s latest complaints data might seem like ‘more of the same’ at headline-level, but for banking and credit card organisations, rising resolution times and backlogs are piling on more handling costs, and increasing the risk of customer churn.

Closures within 3-days are trending downwards (~3% fall between H1-23 and H2), and whilst this has fluctuated since 2020, we’ve seen the trend shift more towards a decline in 2023. If this continues throughout 2024, we could see the majority of banking and credit card complaints taking longer than 3-days to resolve.

With the second half of 2024 fast approaching, improving complaints handling can be key to accelerating closures, focussing on four areas – People, Process, System, and Governance.

During H2-23, some banks saw a ~20% annual increase in complaints taking longer than 8-weeks to resolve, suggesting managing backlogs could become increasingly strenuous, if action isn’t taken to gain back control.

Encouraging agent efficiency in a complex environment for complaints

Improving options available to complaint handling agents can be one of the quickest routes to accelerating closures, particularly in relation to escalations and live support. Are collaborations between customer service and central functions established and reliable? Do you have formal metrics in place to review performance and identify improvement initiatives?

Introducing a support network of experienced specialists into departments with agents can also be beneficial. This network can play the role of advisors, rather than an outlet to hand the complaint over to, which encourages a culture of learning and upskilling – improving an agent’s ability to resolve complaints in future.

The financial sector is extremely complicated and intricate. We’re seeing complaints become more and more complex, particularly since the introduction of Consumer Duty. Your training model may be industry-leading, but even the highest performing agents could forget about rare types of complaints, and how they should be handled.

Therefore, an easy-to-use library of financial information is a key requirement for agents, allowing them to provide the correct information to customers in a timely manner. If you have this documentation in place, is it easy to find, understand, and update? Utilising categorisation, with smart search functionality, is also crucial for enhancing internal complaints maturity.

Leveraging data capabilities to address growing backlogs

One of the main drivers of process inefficiency is the inability for agents to resolve the complaint themselves, and with more people touching a case, the longer it will take to resolve. When did you last review the level of autonomy given to agents? Opportunities to increase this should be considered in the interest of accelerating closures. If this isn’t realistic, can an escalated agent (with increased permissions) be assigned to work closely within the team, to advise on and/or approve decisions?

If a case is required to be sent to another department, such as Tech, then a service-level agreement (SLA) is a must. Agents need to know when to expect a resolution to the escalation, both so they can manage customer expectations, and so there’s no requirement for ‘housekeeping’ duties, monitoring the status of the request. SLA’s can also be used to hold other areas of the business accountable for delivery, with metrics to monitor internal performance.

In addition to this, utilising the abundance of data available within organisations today is crucial to accelerating closures. For example, if there’s a growing backlog, is one area of the complaints function performing slower than others? Is there an area with higher attrition than elsewhere, or perhaps one area is receiving more complaints about their own agents? There must be a formal reporting process in place for complaint trends, flowing through to leadership. Distributing this data frequently, with a trend analysis report, can be pivotal in unlocking ‘weak links’ within the process, before they can have a detrimental impact upon handling costs.

As systems evolve, so should their role in complaint handling teams

Agents will be using various systems for the majority of their working day. For many banks and credit card issuers, legacy systems are still being used due to the complexity of the business. Legacy systems are notoriously difficult to navigate, often not overly user-friendly and very slow to process requests.

If agents are required to continually switch between systems to find different pieces of information, this increases not only resolution times, but also the risk of mistakes due to the variety of systems involved.

Alongside efficiency gains, those using fit-for-purpose systems have access to a plethora of data, which can be fed into business decisions, trend reports, and KPI reviews. How effectively this data is handled, and the insights generated as a result, will determine its impact in driving meaningful change. If you’re operating multiple systems, are they well integrated to the level where analysis and trends are easy to access? Without this insight, data only provides a snapshot of a specific time in the complaints function.

Whether you’re still operating a legacy system in some capacity, or have successfully transitioned, action can be taken to maximise its impact on resolutions.

Incorporating automations into these systems is a great example. Leading complaints functions will be utilising this for instances such as sending standard comms whenever a complaint is acknowledged, or informing customers that there’s no update to give, as well as adding collections blocks to accounts when a complaint is opened.

Keeping complaints agents central to change

As you evolve and improve the complaints function, it’s important to view agents as stakeholders in the overall change process. It should be easy to inform them of the changes impacting their areas, as well as larger organisational developments. An agent should also feel empowered to recommend changes via a feedback channel, and be the champion of the change should it be approved, maybe with a reward incentive too.

Again, with agents being the stakeholders of changes going through the business, their requirements should be fully considered, with agents even being involved in focus groups and testing if necessary. Despite your best intentions, a poorly planned change could negatively impact the productivity of agents, having an adverse effect on resolution times and backlog management.

Complaints are a problem that won’t go away any time soon for the Financial Sector. Through our complaints maturity assessment offering, we’re helping organisations to review the effectiveness of their complaints handling approach, and deliver meaningful improvements within the operation.

If you’d like to know more on how we can help, contact Jonathan Paton.

Jonathan Paton

Senior Manager

Jon specialises in Customer Operations leadership, customer contact, and operational service delivery transformation/improvement.

View Profile