Early signs of improvement were seen in the FCA’s latest Financial Lives survey. Optimistic, yes, but this feeling can only be cautious when 14.6m (28%) people aren’t coping financially, or finding it difficult.

Compared to pre- cost-of-living crisis, ~2m more customers are struggling to keep up with bills and credit commitments, reminding us how significant the shift in circumstances has been since 2020. And yet despite this, the FCA continues to highlight the ineffectiveness of support for those in difficulty, with over half of all customers (54%) saying they haven’t found themselves in a better position when receiving help from their provider.

All of this points to the ongoing need for proactive, tailored support for customers in difficult and vulnerable situations. Looking closer at the survey data shows us which customer segments are struggling the most, and later in this update, we outline the emerging techniques that firms are using to deliver effective support.

Survey findings reinforce FCA’s vulnerability focus

Unsurprisingly, respondents from groups with elements of vulnerability, including low financial resilience and caring responsibilities, were much more likely to state they were not coping at all or finding it very difficult to cope.

Reflecting broader economic changes and accommodation costs, renters also notably stood out compared to other housing tenure groups such as mortgage owners or those who own their property outright.

This comes following last month’s announcement from the FCA, signalling the start of their review into how well firms are responding to vulnerable customers, with service and communications to be put under scrutiny.

The techniques covered later in this update will help firms to cross-check their customer service and collections approach against best practice, whilst our blog on vulnerability in product design explores the other side of the challenge.

Missed credit payments rising, and utility bills remain major challenge

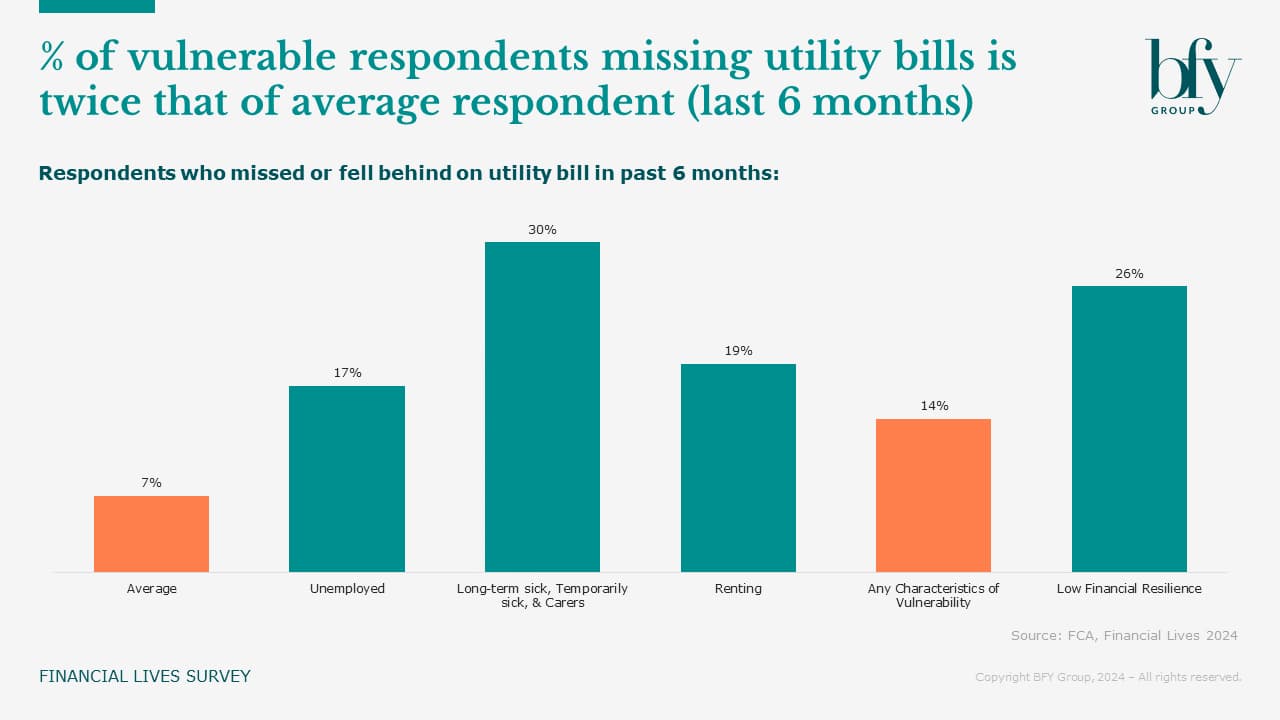

Several customer segments also buck the trend of improving circumstances over the last 12 months. Rates of ability to financially cope have worsened in certain geographies, notably Northern Ireland, the North East and East Midlands, whilst respondents identifying as self employed also appear to be struggling more compared to their employed and retired counterparts.

These discrepancies are also highly prevalent in customers’ ability to pay bills, where all categories mentioned above had rates of missed utility payments at least double that of the national average. Although rates of missed payments on credit cards have increased in many of these categories, utility bills remain the most likely to not be paid, highlighted recently in our energy practice.

Proactive and personalised support – What next?

Segmented collections paths are vital to ensure that customers who need it receive tailored, appropriate treatment for their circumstances.

Emerging techniques include:

- Combining new data sources, like some of the publicly available demographic data used in the FCA survey, with existing data such as customer postcodes to deliver segmented customer journeys

- Market leading firms are using AI and machine learning to make their collections processes more data driven, and segmenting customer journeys on an increasingly granular level

- Using machine learning to improve predelinquency and early collections processes, with the aim of enhancing collections performance

Alongside this, proactive vulnerability identification and communication is essential for supporting customers earlier and limiting arrears.

This means:

- Text and voice analytics can help businesses to dramatically improve vulnerability detection

- Clear, tailored communications at the right time, and in the right format for customers, can uplift performance and response rates across all types of journeys

- Given the crystal-clear link between vulnerability and financial struggles, it’s vital to assess this before and during collections processes, especially to ensure regulatory conditions are fully satisfied

As the cost-of-living crisis continues to create payment difficulties for customers, being dependent on credit is likely to remain the norm for certain segments, leaving the financial sector in a challenging position.

Focussing on delivering the right outcomes, and signposting this as early as possible, should remain the priority, utilising the approaches above where possible.

If you’d like to know more about offering proactive, tailored support, and the outcomes its delivered for our clients, contact John Scott.

John Scott

Manager

John partners with our clients to deliver transformation and performance improvement - focussing on operational improvement, strategic and regulatory programme delivery, and process design/implementation.

View Profile