We’re starting to see murmurs of activity in what’s been a very low-activity switching market.

And the pace looks set to increase following Ofgem’s April price cap, alongside the cessation of the market stabilisation charge – which previously discouraged suppliers from offering switching incentives.

Hugely expanded data collection in recent years, through smart meters and half hourly settlements, now provides an opportunity for suppliers to offer increasingly personalised energy packages, and actively target segments of the market.

We expect to see the emergence of increasingly innovative tariffs, some already seen with time-of-use (TOU) and electric vehicles (EVs). But, this risks translating into more complexity for customers; many of whom already feel unable to evaluate the future costs of different energy tariffs.

This blog assesses the impact of tariff complexity on customer choice in today’s market, looking closer at the factors driving it, and the opportunities for suppliers to provide greater clarity – with Market-Wide Half Hourly Settlements (MHHS) on the horizon.

Future Price Caps could bring more complexity

Ofgem has acknowledged the evolving energy tariff landscape and is in discussions about the future of the price cap. This could lead to a more dynamic cap, with time-of-use dependent unit rates to encourage consumer flexibility, and the potential for a targeted cap, which could be based on factors such as vulnerability.

If introduced, these changes will add to the existing complexity for customers, so it’s crucial that suppliers are supporting them in making informed decisions. This support is a necessity for today, as much as the future, as suppliers look to attract and retain customers through innovative propositions.

Why are tariff decisions difficult for energy customers?

Many consumers already struggle to evaluate the future costs of various tariff options.

We attribute this to three reasons:

1) Standard variable tariffs and their associated costs are misunderstood

The cost of remaining on the SVT for the next 12 months is unknown, as it’s based on a fluctuating wholesale price, and four future price caps. Across consumers, there’s a lack of understanding on how the price cap is calculated, and although widely advertised, the figure is illustrative, representing a notional annual spend.

Therefore, it doesn’t accurately represent what the majority of customers will pay.

2) Tariffs on supplier and comparison websites are usually quoted incomparably

There’s significant variation in the way tariffs are quoted and advertised by suppliers, making comparison tricky. For example, some comparison sites compare costs of tariffs with differing assumed consumption levels. In addition, tariffs are often advertised as ‘beating the price cap’, but this is not necessarily the same as beating the SVT for 12 months and doesn’t guarantee good value.

We also see little translation of unit rates and standing charges into total anticipated cost for the consumer. From a customer’s point of view, this energy tariff market is complicated.

3) Customer guidance is generic and can misidentify the cheapest deal

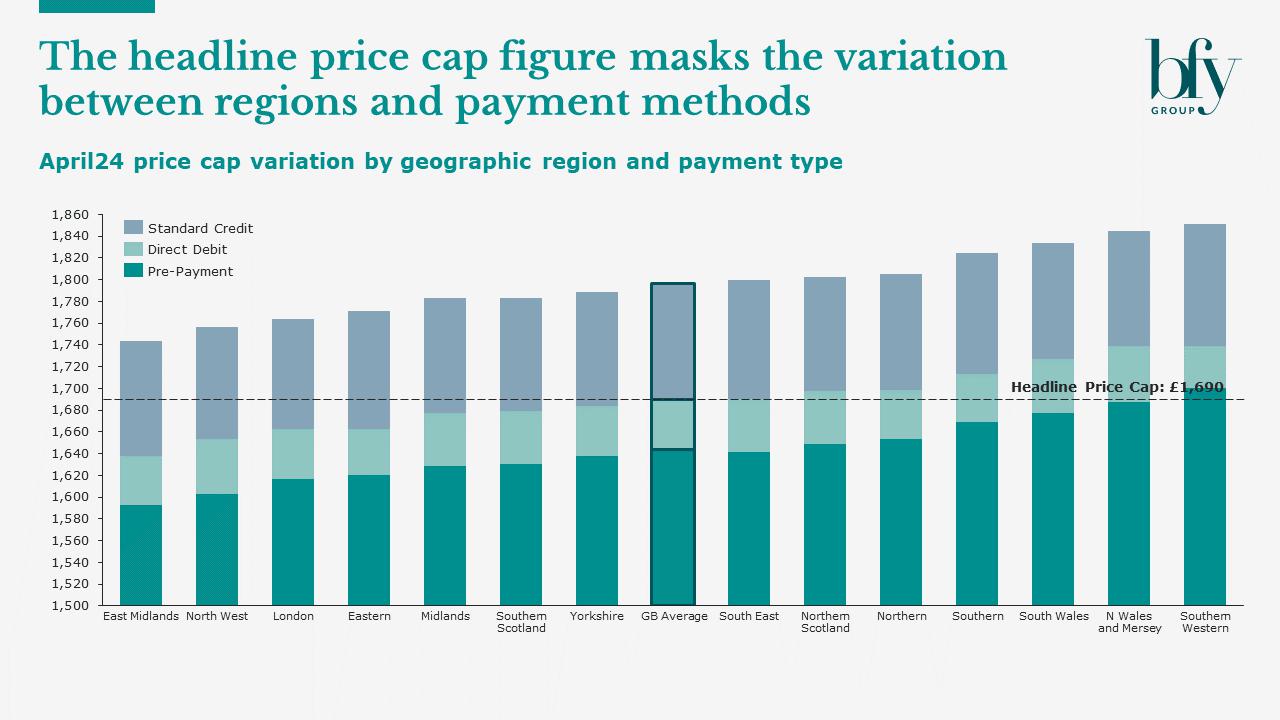

One size does not fit all. Guidance to fix relative to the price cap ignores differentiators such as geographical region, or payment method of the consumer. So commonly quoted descriptions of individual tariffs, as “x% less” than the price cap, is only correct for the national average consumption when assuming payment by direct debit.

Similarly, quotes of savings on TOU tariffs can be misleading, and depend on assumed future consumption.

EV tariffs are evidence of a complex switching market

These 3 issues become more apparent when considering the range of innovative tariffs that are available to electricity consumers – particularly when comparing available EV tariffs. With potential savings depending on levels of off-peak consumption (where rates are lower), it’s not as simple as assuming an EV tariff is the most cost-effective option for an EV owner.

Under the more competitive EV tariffs on the market:

- ~10% of consumption needs to be during off-peak hours to make the tariff worthwhile

- A proportion greater than 10% would bring cost savings relative to the SVT

For context, ‘medium level’ electricity customers consume ~9-11% during off-peak, so adding EV charging into the mix would imply a saving on this tariff. However, the less competitive EV tariffs we analysed showed that the customers would need to consume at least ~23% of their overall electricity usage during off-peak hours to make a saving. Furthermore some EV tariffs don’t allow any non-charging consumption at the off-peak rate.

Other notable scenarios include:

- High-base level electricity consumers, with low annual mileage – most EV charging would be needed in off-peak hours to ensure value for money

- Low-base level electricity consumers, OR those with high mileage – EV tariffs are likely to be most economical, even if not all charging is off-peak

Overall, this shows just how much the consumption profile of a consumer can influence the cost effectiveness of tariffs, and the complexity involved in making the right choice.

Opportunities for clarity – Smart and Half Hourly Settlements

At present, most customers don’t understand their consumption habits well enough to choose the most cost-effective tariff – meaning there’s an enormous opportunity in the market.

The smart meter roll out reached c.61% by the end of 2023, giving consumers and suppliers increased access to accurate energy consumption patterns. In addition, the introduction of Market-Wide Half Hourly Settlements (MHHS) means both customers and suppliers will be exposed to their true underlying energy profile throughout the day.

As a result, this wealth of data could be leveraged to personalise offerings and support customers in making informed decisions, based on their individual needs and consumption. There’s a huge opportunity to re-engage customers and increase awareness of their consumption behaviours and its associated cost.

With successful communication from suppliers, this information should help customers make smarter energy consumption decisions, and actively participate in managing their consumption profile through consumption shifting, uptake of TOU tariffs, electric vehicles, and smart home appliances.

Suppliers have a genuine opportunity to use unique insights to build trust with customers. This should enable consumers to reduce their energy costs, whilst helping to build a flexible, low-carbon energy system that’s both affordable and secure.

But there is a risk that increased information leads to increased confusion, and translating usage data into suitable customer offerings will come with operational and system challenges and costs.

In an energy market that’s becoming increasingly innovative, those that utilise data effectively, and prioritise clarity for the customer, will come out on top.

If you’d like to know more about the role of energy suppliers in customer switching, and the opportunities surrounding MHHS, contact Tom Bromwich or Charlotte Warman.

Matt Turner-Tait

Senior Manager

Matt lead clients through key strategic projects exploring growth opportunities, business models, competitive advantage, and mergers & acquisitions.

View Profile