The latest government stats on smart meters paint a familiar picture: progress is being made, but not fast enough, and certainly not evenly.

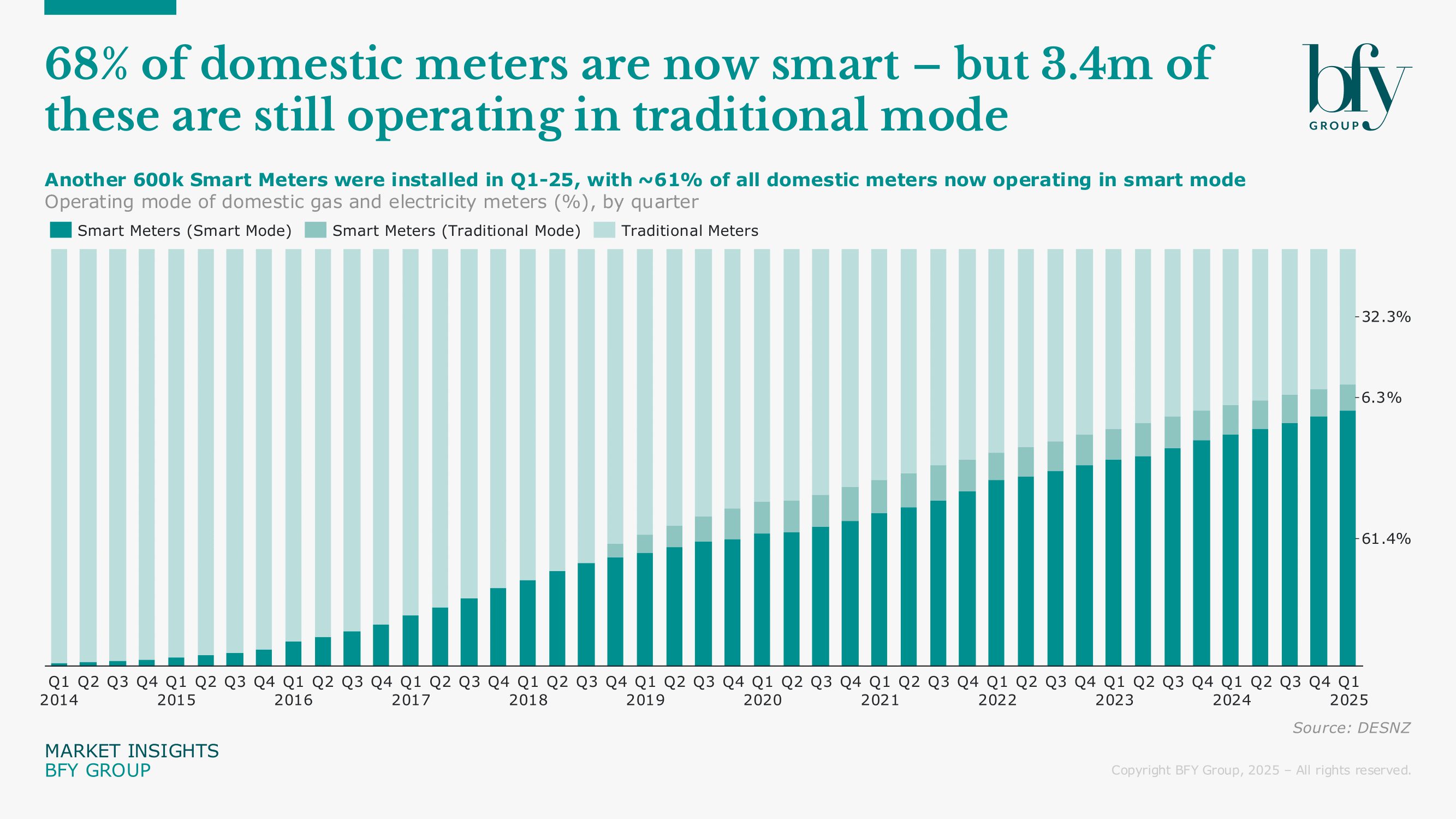

As of March 2025, date from the Department for Energy Security and Net Zero (DESNZ) shows 39m smart and advanced meters have been installed across Great Britain, covering around 67% of ‘all meters’ (domestic and non domestic – 68% for domestic alone).

Ofgem’s new open consultation is refocusing suppliers on two priorities. First, ensuring smart meters operating in traditional mode are restored to smart mode within 90 days. Second, taking “all reasonable steps” to complete the rollout to all domestic customers by 2030. We believe there’s still a window of opportunity to meet smart targets - but it will take more than simply accelerating installation rates.

Installation numbers are up, but momentum is slipping

According to DESNZ, large suppliers installed a total of 720k smart and advanced meters in Q1 2025 across domestic and non-domestic properties (600k for domestic alone). This was a modest increase on the previous quarter. While the overall number is encouraging, there are signs that the rollout is slowing in some parts of the country.

With Ofgem actively monitoring performance, there’s a real risk of missing the initial government target - 74.5% of households with a smart meter by the end of 2025. Hitting that goal, and then progressing towards the 2030 target, will rely on improving the quality of installs, not just the quantity.

Having a meter installed is not the same as going smart

One of the biggest issues we continue to see across the market is the gap between installation and actual smart operation. The latest update from DESNZ shows that 91% of all installed smart meters are operating in smart mode. That still leaves over 3m ‘smart’ meters either in traditional mode or not functioning as intended, and this number is being propped up by non-domestic meters.

This isn’t a new problem, but it’s becoming more visible. As we said in our previous article "Installation is only half the battle", getting kit into homes and businesses is only step one. Recommissioning, ongoing connectivity and customer understanding are just as important.

Without focus on those areas, there’s a real risk of wasted investment and regulatory non-compliance.

Regional gaps still holding back national progress

The latest government figures show that coverage continues to vary significantly across regions. At the end of March 2025, 66% of domestic electricity meters and 56% of gas meters were operating in smart mode across Great Britain. When including meters operating in traditional mode, this rises to 70% for electricity and 65% for gas.

DESNZ data also highlights regional variation in smart meter rollout performance. Some local authorities, including London, are significantly below the national average of 68%, with coverage as low as 60%. The report also notes differences between rural and urban areas, as well as across nations, with rollout rates at 71% in England, 67% in Wales and 57% in Scotland.

Effective rollout planning depends on more than logistics. It requires clear focus. Too many rollout plans still rely on broad national targets, rather than using local-level data to identify underperforming areas and direct field teams more effectively.

Four things suppliers can still do differently

As we’ve seen when supporting clients through these challenges, there are still practical levers you can pull. Here are four that can make a difference right now:

1) Fix what’s already there

Smart meters not operating in smart mode are low-hanging fruit. Proactive recommissioning, supported by better use of DCC alerts and field intelligence, can lift smart coverage quickly without needing to install new devices.

2) Improve field productivity and better integrate with Customer Contact teams

Reducing no-access rates, improving job routing and giving field teams better data can drive up daily outputs and help meet delivery targets. Customer service teams need access to live install schedules to coordinate efficiently and make real time changes.

3) Strengthen customer follow-up

Smart meters are not delivering value unless customers know how to use them. That means getting In Home Displays (IHDs) working, helping people understand their usage data and making smart tariffs more visible and accessible.

4) Region-Specific Plans

Building region-specific plans using smart meter data, DCC insights and customer segmentation will result in more efficient field operations, better engagement and higher conversion to smart mode.

What should energy suppliers be doing now?

Now is the time to ask some hard questions. Is your smart delivery plan built around installations or outcomes? Are you treating all regions equally or focusing where the impact will be greatest? And are your field teams and customer operations teams working from the same playbook?

With the 2025 target approaching, and the new consultation adding greater obligations and oversight beyond that, the most forward-thinking suppliers will:

- Set more granular targets for smart mode performance, not just installs

- Focus rollout on underperforming regions using local data

- Invest in digital tools to monitor progress across field and commissioning

- Build smart engagement into everyday customer servicing journeys, not bolt it on afterwards

- Treat recommissioning as a core delivery metric, not a clean-up task

Closing the Gap: How BFY can help

At BFY, we’ve helped suppliers across the industry turn underperformance around. This includes developing regional rollout strategies, improving field efficiency, redesigning customer journeys and tackling legacy issues in the smart meter estate.

We know what’s working, what isn’t, and what Ofgem expects to see. More importantly, we know how to bring the right people, processes and data together to deliver results.

If you’re concerned about missing the initial 2025 target and potential Ofgem sanctions - whether installations are slowing, smart mode performance is falling behind or regional gaps are holding you back – we’re here to help.

For more on how we can support you and what needs to happen next, contact Jonathan Paton or Jonathan Holland.

Jonathan Paton

Senior Manager

Jon specialises in Customer Operations leadership, customer contact, and operational service delivery transformation/improvement.

View Profile