Now that the April sales round has passed, further pressure is building in the B2B market.

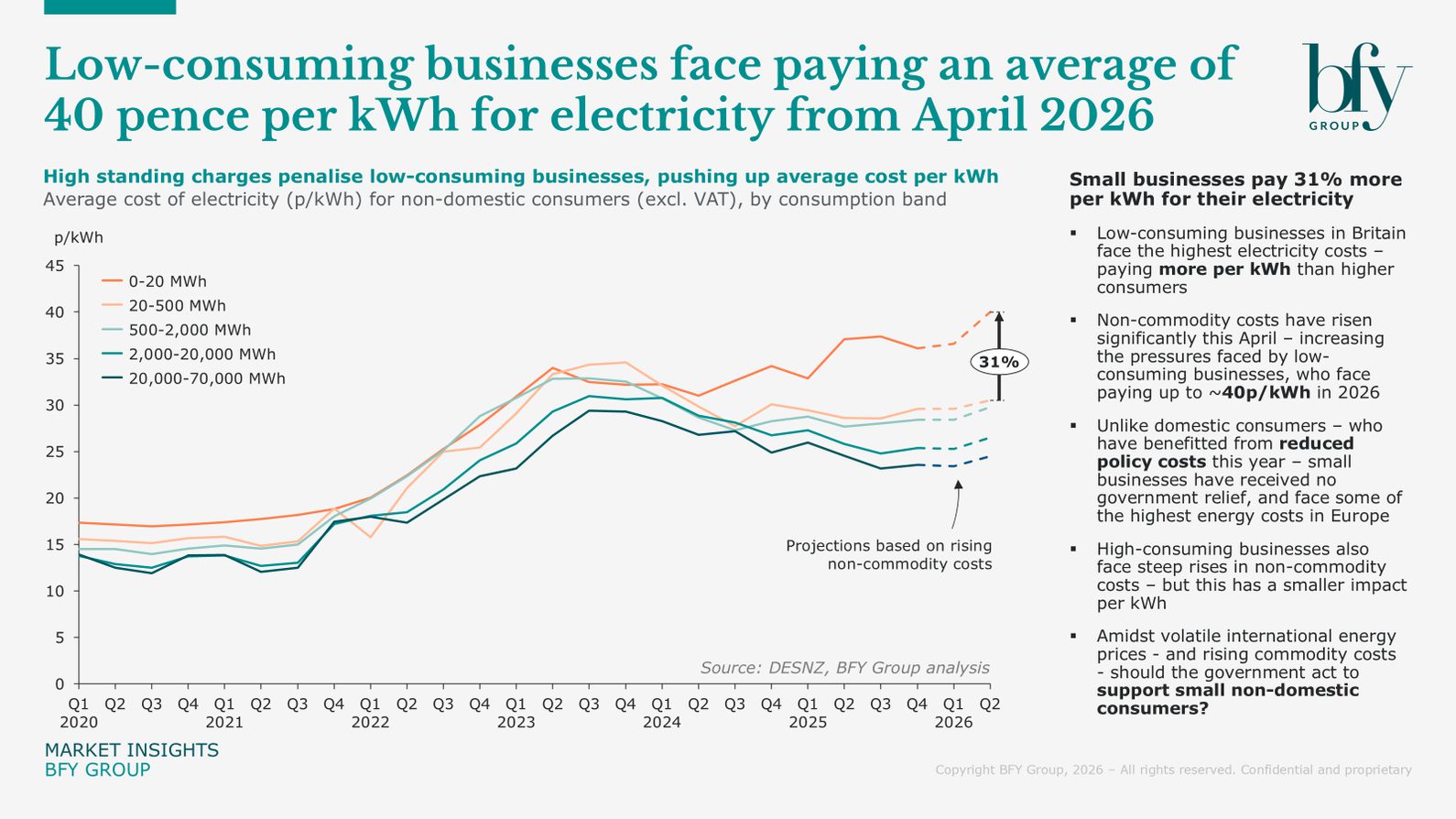

Our analysis of DESNZ data reveals a widening disparity in the average cost of energy. Small, low-consuming businesses are facing some of the highest electricity costs in Europe, with average prices projected to reach ~40p/kWh this year. These businesses are currently paying 31% more per kWh than their higher-consuming counterparts.

While much of the national conversation has focused on domestic relief, small non-domestic customers haven't seen the same level of support, despite facing these significantly higher unit costs.

The drivers of disparity

The widening gap’s largely the result of two factors.

First, the sharp rise in non-commodity charges that took effect on April 1st. While network costs have increased across the board, the impact’s disproportionately felt by low-consumers. Larger industrial consumers can often absorb these rises more effectively on a per-unit basis, whereas fixed costs and standing charges make up a greater proportion of overall energy costs for SMEs.

Second, there’s a clear divergence in policy relief. Unlike domestic consumers who’ve benefited from a reduction in policy costs this year, small businesses haven't received any such government intervention. On top of this, they remain exposed to volatile international energy prices and rising commodity costs, placing further pressure on SME customers.

Navigating the commercial impact

For suppliers, these rising SME costs create a difficult ripple effect across both commercial and operational processes:

- Customer Affordability: Rising bills increase the risk of bad debt and credit stress within the SME portfolio

- Servicing Demand: Increases in inbound contact as businesses seek clarity on their bills or want to renegotiate

- Operational Strain: Increased quoting complexity and reliance on manual intervention can impact efficiency, consistency, and accuracy

Navigating this environment often means looking beyond reactive price monitoring alone. For many suppliers, these types of pressures are increasing the importance of stronger forecasting, clearer product positioning, and more consistent operational processes across SME portfolios.

As we move into the October round, success will likely depend not just on price competition alone, but also how well suppliers help customers manage customer journeys, operational readiness, and commercial execution. This includes sharpening forecasting, improving product clarity, and empowering sales teams to move from transactional quoting to advisory-led conversations.

You can read more here on why operating rhythm is becoming a key differentiator in B2B energy sales.

If you’d like to discuss the data behind this analysis or how we’re helping B2B suppliers strengthen their commercial performance, contact Hannah Sword.

Hannah Sword

Director

Hannah leads client engagements, striving to ensure clients gain significant value and benefits and from the work we deliver.

View Profile